Finova

The mortgage accessibility crisis has become America's invisible housing barrier, with 2023 Federal Reserve data showing 43% of mortgage applications now face rejection due to the affordable housing crisis. As Zillow reports median home prices climbing 19.8% since 2020 while wages grew just 4.7%, this analysis examines the collision of housing shortages, lending restrictions, and the housing affordability index through a critical rent vs own analysis framework.

FHFA data reveals a 63% home price surge in competitive markets like Austin (TX) and Boise (ID) since 2019, dramatically outpacing the 14% wage growth documented by the Bureau of Labor Statistics. In Miami-Dade County, where median incomes stagnate at $56,000, the NAR reports mortgage accessibility has declined 37% since Q2 021 due to price escalation.

The NAHB's 2023 deficit analysis shows Phoenix needs 132,000 additional units to meet demand, while Seattle requires 88,000. This shortage creates bidding wars where 72% of listings receive multiple offers (Redfin Q3 2023), forcing lenders to implement stricter mortgage accessibility challenges in the US affordable housing crisis.

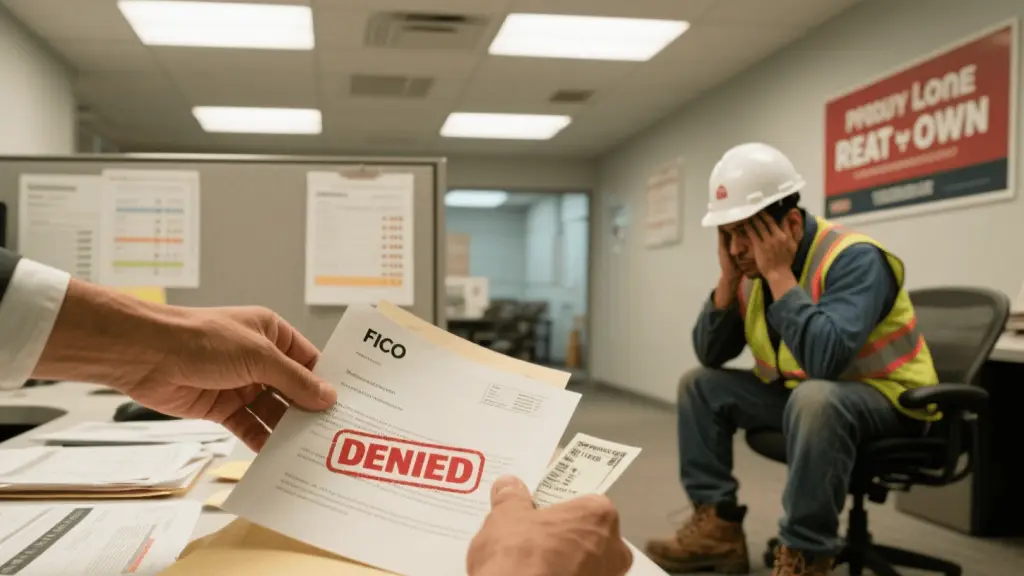

Urban Institute's 2023 lending analysis reveals conventional loans now require average FICO scores of 758 (up from 713 in 2019), while FHA loans demand 686 (versus 670 pre-pandemic). The housing affordability index shows these credit barriers exclude 28% of potential first-time buyers nationwide.

While FHA loans assist 83,000 buyers monthly (HUD 2023), their $472,000 limit in high-cost areas falls $328,000 short of the $800,000 median in markets like San Diego. States like Massachusetts now supplement with "ONE Mortgage" programs offering 3% down payments to combat mortgage accessibility erosion.

NAR's Q4 2023 housing affordability index reveals alarming trends: Los Angeles (54), San Francisco (48), and New York (62) all score below the 100 threshold. This means median-income families can afford just half the median-priced home in these markets, creating unprecedented mortgage accessibility challenges in the US affordable housing crisis.

Pittsburgh (156), Oklahoma City (142), and Memphis (138) lead in affordability per NAR data, while coastal metros struggle. The rent vs own analysis becomes critical here - in high-index cities, buying saves $387/month versus renting (Zillow 2023), whereas in low-index cities, renting averages $423 cheaper.

Zillow's 2023 rent vs own analysis shows buying now takes 5.3 years to break even nationally versus renting - up from 3.1 years in 2019. In expensive markets like San Jose, the breakeven point extends to 9.8 years due to high prices and property taxes impacting mortgage accessibility.

Case studies from Denver show tech workers saving 22% more in retirement accounts by renting downtown versus buying suburbs. Conversely, Birmingham homeowners build equity 3.2x faster than renters (NAR 2023), proving location-specific housing affordability index outcomes.

The mortgage accessibility landscape requires urgent solutions as the affordable housing crisis persists. With 58% of millennials now delaying homeownership (Pew Research 2023), policymakers must address zoning laws (currently restricting 75% of residential land per Brookings) and expand FHA limits to restore the housing affordability index balance.

Disclaimer: This content regarding is for informational purposes only and does not constitute financial, legal, or professional advice. Consult qualified experts before making housing decisions. The author and publisher disclaim liability for any actions taken based on this information.

Thompson, L.

|

2025.08.07